Mastering Debt Reduction: High-Interest Credit Card Strategies for 2026

Mastering Debt Reduction: High-Interest Credit Card Strategies for 2026

Are you tired of the endless cycle of high-interest credit card debt? Do you dream of a future where your finances are firmly under your control? The good news is that achieving financial freedom is within reach, and 2026 can be your year to make significant strides. This comprehensive guide will explore powerful debt reduction strategies specifically tailored to help you pay off high-interest credit card debt by 20% within the next year. We’ll delve into actionable plans, practical tips, and the mindset shifts necessary to transform your financial landscape.

Understanding Your Debt Landscape: The First Step Towards Freedom

Before you can conquer your debt, you must first understand it. Many people avoid looking at their credit card statements, but this avoidance only perpetuates the problem. The first crucial step in any effective debt reduction strategy is to gather all your credit card statements and list out every single debt. For each card, note down:

- The total balance owed.

- The interest rate (APR).

- The minimum monthly payment.

This exercise might feel daunting, but it provides a clear picture of your financial situation. High-interest credit card debt is particularly insidious because a significant portion of your minimum payment often goes towards interest rather than the principal, making it feel like you’re running in place. Identifying these high-interest accounts is paramount as they will be your primary targets.

Why Focus on High-Interest Debt?

When implementing debt reduction strategies, prioritizing high-interest debt saves you the most money in the long run. The higher the interest rate, the more expensive the debt becomes over time. By tackling these first, you reduce the overall cost of your debt and free up more money to pay down other balances faster. This approach, often called the ‘debt avalanche’ method, is mathematically the most efficient way to get out of debt.

Setting Realistic Goals: The 20% Reduction by 2026 Target

Our goal is ambitious yet achievable: to reduce your high-interest credit card debt by 20% within the next year, paving the way for a debt-free 2026. Why 20%? Because it’s a significant enough chunk to make a noticeable difference, provide motivation, and build momentum without being so overwhelming that it feels impossible. To break this down, calculate 20% of your total high-interest credit card debt. This is your target amount. Now, divide that by 12 months to see how much you need to pay down each month, on average, beyond your minimum payments.

For example, if you have $10,000 in high-interest credit card debt, your target is to reduce it by $2,000. This means finding an extra $167 per month to put towards your debt. This number might seem more manageable when broken down.

Crafting Your Budget: The Foundation of Any Debt Reduction Strategy

You cannot effectively implement debt reduction strategies without a clear understanding of where your money is going. A budget is not about restriction; it’s about control and intentional spending. Start by tracking all your income and expenses for at least one month. You can use:

- Budgeting apps (Mint, YNAB, Personal Capital).

- Spreadsheets (Google Sheets, Excel).

- A simple pen and paper.

Categorize your expenses into fixed (rent, loan payments) and variable (groceries, entertainment). Be brutally honest with yourself about your spending habits. Often, you’ll uncover ‘money leaks’ – small, regular expenses that add up significantly over time. Identifying these areas is crucial for freeing up funds that can be redirected towards debt repayment.

Finding Extra Funds: Beyond the Obvious

Once you have a clear budget, look for opportunities to cut back. This might involve:

- Reducing discretionary spending: Eating out less, canceling unused subscriptions, finding cheaper entertainment options.

- Negotiating bills: Call your internet, cable, or insurance providers to see if you can get a better rate.

- Selling unused items: Declutter your home and sell items on online marketplaces.

- Temporary side hustles: Consider taking on a part-time job or freelancing for a few months to boost your income.

Every extra dollar you can free up is a dollar that can be used to accelerate your debt reduction strategies.

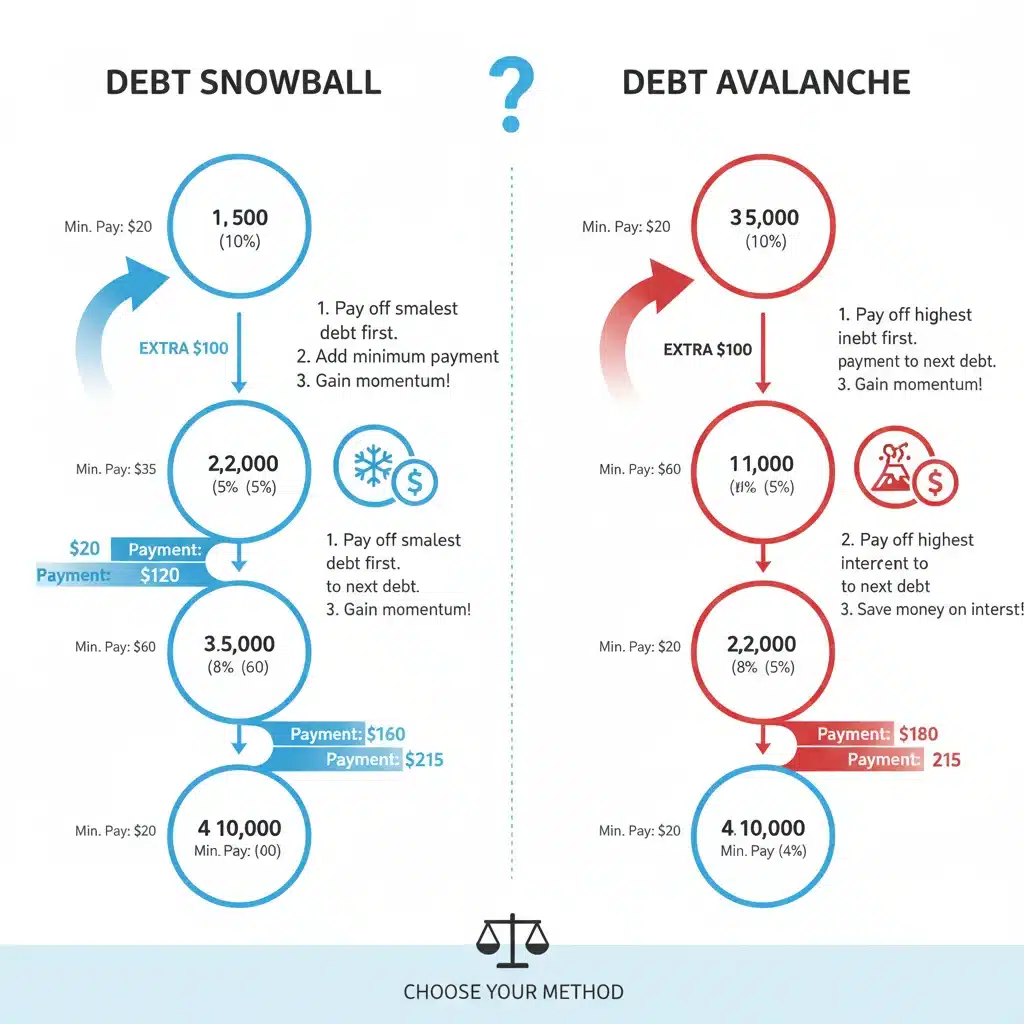

Choosing Your Debt Repayment Method: Avalanche vs. Snowball

When it comes to paying down multiple debts, two popular debt reduction strategies stand out: the debt avalanche and the debt snowball. Both are effective, but they cater to different psychological and financial preferences.

The Debt Avalanche Method

This method focuses on paying off debts with the highest interest rates first, while making minimum payments on all other debts. Once the highest-interest debt is paid off, you take the money you were paying on that debt and add it to the payment of the next highest-interest debt. This continues until all debts are paid. The debt avalanche saves you the most money in interest charges and is mathematically the most efficient strategy.

The Debt Snowball Method

The debt snowball method prioritizes paying off the smallest debt first, regardless of its interest rate. You make minimum payments on all other debts, and once the smallest debt is paid off, you roll that payment amount into the next smallest debt. This creates a ‘snowball’ effect, building momentum and motivation as you quickly eliminate smaller balances. While it may cost slightly more in interest than the avalanche method, the psychological wins can be incredibly powerful for those who need frequent encouragement.

For high-interest credit card debt, the debt avalanche is often recommended due to its cost-saving benefits. However, if you feel easily discouraged and need quick wins to stay motivated, the debt snowball might be a better fit to kickstart your debt reduction strategies.

Leveraging Financial Tools and Resources

Beyond budgeting and repayment methods, several financial tools and resources can significantly boost your debt reduction strategies.

1. Balance Transfer Credit Cards

If you have good credit, you might qualify for a balance transfer credit card with a 0% introductory APR. This allows you to move your high-interest credit card debt to a new card and pay no interest for a period, typically 12 to 21 months. This breathing room can be invaluable for making significant progress on your principal balance. Be mindful of balance transfer fees (usually 3-5% of the transferred amount) and ensure you have a plan to pay off the transferred balance before the introductory period ends and the regular APR kicks in.

2. Personal Loans for Debt Consolidation

A personal loan can be another effective tool. By taking out a single loan with a lower, fixed interest rate, you can consolidate multiple high-interest credit card debts into one monthly payment. This simplifies your finances and can save you a substantial amount in interest over time. Look for reputable lenders and compare interest rates and fees carefully.

3. Debt Management Plans (DMPs)

If you’re struggling to manage your debt on your own, a non-profit credit counseling agency can help. They can set up a Debt Management Plan (DMP) where they negotiate with your creditors for lower interest rates and a single, affordable monthly payment. While DMPs can be very effective, they might require you to close your credit card accounts and can have a minor, temporary impact on your credit score. However, the long-term benefits of becoming debt-free often outweigh these drawbacks.

4. Negotiating with Creditors

Don’t underestimate the power of direct communication. Sometimes, if you’re experiencing financial hardship, your credit card company might be willing to work with you. They may offer a temporary reduction in interest rates, waive late fees, or even set up a temporary payment plan. It never hurts to call and explain your situation.

Building a Strong Financial Foundation for 2026 and Beyond

While the immediate goal is to reduce debt, true financial freedom involves building sustainable habits. These foundational elements will ensure your debt reduction strategies lead to lasting success.

A. Emergency Fund: Your Financial Safety Net

One of the primary reasons people fall into credit card debt is unexpected expenses. A robust emergency fund acts as a buffer, preventing you from resorting to high-interest credit cards when life throws a curveball. Aim to save at least three to six months’ worth of essential living expenses in a separate, easily accessible savings account. Even while paying off debt, try to build a small starter emergency fund (e.g., $1,000) first, then focus aggressively on debt, and finally, build your full emergency fund.

B. Smart Credit Card Usage

Once you’ve made significant progress on your debt, it’s crucial to change your relationship with credit cards. If you choose to keep them, use them responsibly: pay off your balance in full every month to avoid interest charges, and only charge what you can afford. Consider using them for specific categories where you earn rewards, but treat them like a debit card – only spend money you already have.

C. Continuous Financial Education

The world of personal finance is constantly evolving. Stay informed by reading books, listening to podcasts, and following reputable financial blogs. The more you learn, the better equipped you’ll be to make smart financial decisions and adapt your debt reduction strategies as your circumstances change.

Overcoming Challenges and Staying Motivated

The journey to debt freedom is rarely linear. You’ll encounter challenges, setbacks, and moments of discouragement. Here’s how to navigate them:

- Celebrate Small Wins: Acknowledge every milestone, no matter how small. Paying off a card, hitting a savings goal, or even just sticking to your budget for a month are all reasons to celebrate.

- Stay Accountable: Share your goals with a trusted friend, family member, or join an online community. Having someone to hold you accountable can make a huge difference.

- Automate Payments: Set up automatic payments for at least the minimum amounts to avoid late fees and ensure consistent progress.

- Review and Adjust: Your budget and debt repayment plan aren’t set in stone. Life happens. Review your progress regularly and adjust your plan as needed.

- Focus on the ‘Why’: Remind yourself why you started this journey. Is it for a stress-free future? To save for a down payment? To travel? Keeping your ultimate goals in mind will fuel your motivation.

The Psychological Impact of Debt Reduction

Beyond the numbers, the psychological benefits of implementing effective debt reduction strategies are immense. Debt can be a heavy burden, leading to stress, anxiety, and even health issues. As you start to see your balances decrease, you’ll experience a profound sense of relief, empowerment, and control over your life. This newfound confidence extends beyond your finances, positively impacting other areas of your life.

Imagine the freedom of not having monthly high-interest payments hanging over your head. Think about the possibilities that open up when more of your income is available for saving, investing, or pursuing your passions. These are the rewards that await you as you diligently apply these debt reduction strategies.

Conclusion: Your Path to a Debt-Reduced 2026

Reducing your high-interest credit card debt by 20% within the next year is an achievable and transformative goal for 2026. It requires commitment, discipline, and a well-thought-out plan. By understanding your debt, creating a realistic budget, choosing an effective repayment method, and leveraging available financial tools, you are setting yourself up for success.

Remember, this is a journey, not a sprint. There will be ups and downs, but with persistence and a clear vision, you can make significant progress towards financial freedom. Start today by taking that first step: gather your statements, analyze your spending, and commit to one of these powerful debt reduction strategies. Your future self will thank you for the financial peace of mind you’ll gain.

Embrace the challenge, stay focused, and look forward to celebrating your progress towards a financially healthier 2026!