Fresh Start Program 2026: Reclaim Federal Student Aid Eligibility Fast

Navigating the complexities of federal student aid can be daunting, especially if you’ve encountered challenges leading to loan default. The good news is that the U.S. Department of Education consistently works to provide pathways for borrowers to regain their financial footing and continue their educational journeys. One such critical initiative is the Fresh Start Program. With significant updates anticipated for 2026, understanding this program is more crucial than ever. This comprehensive guide will delve into the nuances of the Fresh Start Program, outlining what it is, who it benefits, the key updates for 2026, and most importantly, how you can reclaim your eligibility for federal student aid within a remarkable three-month timeframe.

Understanding the Fresh Start Program: A Second Chance for Borrowers

The Fresh Start Program is a temporary initiative designed to assist borrowers whose federal student loans were in default prior to a specific date. Its primary goal is to remove the negative consequences of default, such as wage garnishment, tax refund offsets, and ineligibility for further federal student aid, thereby offering a genuine second chance. This program was initially introduced in response to the economic challenges posed by the COVID-19 pandemic, providing a much-needed lifeline to millions of Americans.

What Does Default Mean for Your Student Loans?

Before diving deeper into the Fresh Start Program, it’s essential to understand what it means for your federal student loans to be in default. Default occurs when you fail to make your loan payments for a specified period, typically 270 days for federal student loans. Once a loan defaults, several severe consequences can ensue:

- Damage to Credit Score: Default is reported to credit bureaus, significantly harming your credit rating and making it difficult to obtain future loans, mortgages, or even rent an apartment.

- Wage Garnishment: The government can seize a portion of your wages without a court order.

- Tax Refund Offset: Your federal and state tax refunds can be withheld to pay down your defaulted loan.

- Loss of Eligibility for Federal Student Aid: This is a major concern for many, as it prevents access to grants, subsidized loans, and other financial assistance for future education.

- Ineligibility for Deferment or Forbearance: You lose access to options that can temporarily pause or reduce your loan payments.

- Collection Fees: Additional fees can be added to your loan balance, increasing your overall debt.

The Fresh Start Program aims to reverse these detrimental effects, offering a path to rehabilitation and renewed financial stability.

Key Updates and Anticipated Changes for the Fresh Start Program in 2026

While the Fresh Start Program has been a temporary measure, discussions and potential legislative actions are ongoing regarding its future and possible extensions or modifications. As we look towards 2026, it’s vital to stay informed about any anticipated changes that could impact your eligibility or the program’s structure. While specific details for 2026 are subject to legislative decisions and Department of Education announcements, here are some areas where updates might occur:

Potential Expansion of Eligibility Criteria

One area of potential change could be the expansion of eligibility criteria. Currently, the program primarily targets loans that defaulted before a certain date. Future iterations might extend this window or include other categories of borrowers facing financial hardship.

Streamlined Application Process

The Department of Education continually seeks to simplify processes for borrowers. We might see further streamlining of the application or reclamation process for the Fresh Start Program, making it even easier for eligible individuals to participate and regain good standing.

Integration with Other Debt Relief Initiatives

As the landscape of student loan policy evolves, there’s a possibility that the Fresh Start Program could be integrated more closely with other debt relief or income-driven repayment (IDR) plans. This could offer a more holistic approach to managing student debt and preventing future defaults.

Focus on Long-Term Financial Literacy

Future updates might also place a greater emphasis on financial literacy and counseling as part of the program, ensuring that borrowers not only exit default but also have the tools and knowledge to manage their finances effectively moving forward. This proactive approach could help prevent a return to default.

It is crucial for borrowers to regularly check the official Federal Student Aid website (StudentAid.gov) for the most up-to-date information regarding the Fresh Start Program and any changes that may take effect in 2026. This will ensure you have accurate and timely information to make informed decisions about your student loans.

Who Qualifies for the Fresh Start Program?

To benefit from the Fresh Start Program, you generally need to meet specific criteria. While these are subject to change, the core requirements typically revolve around the status of your federal student loans:

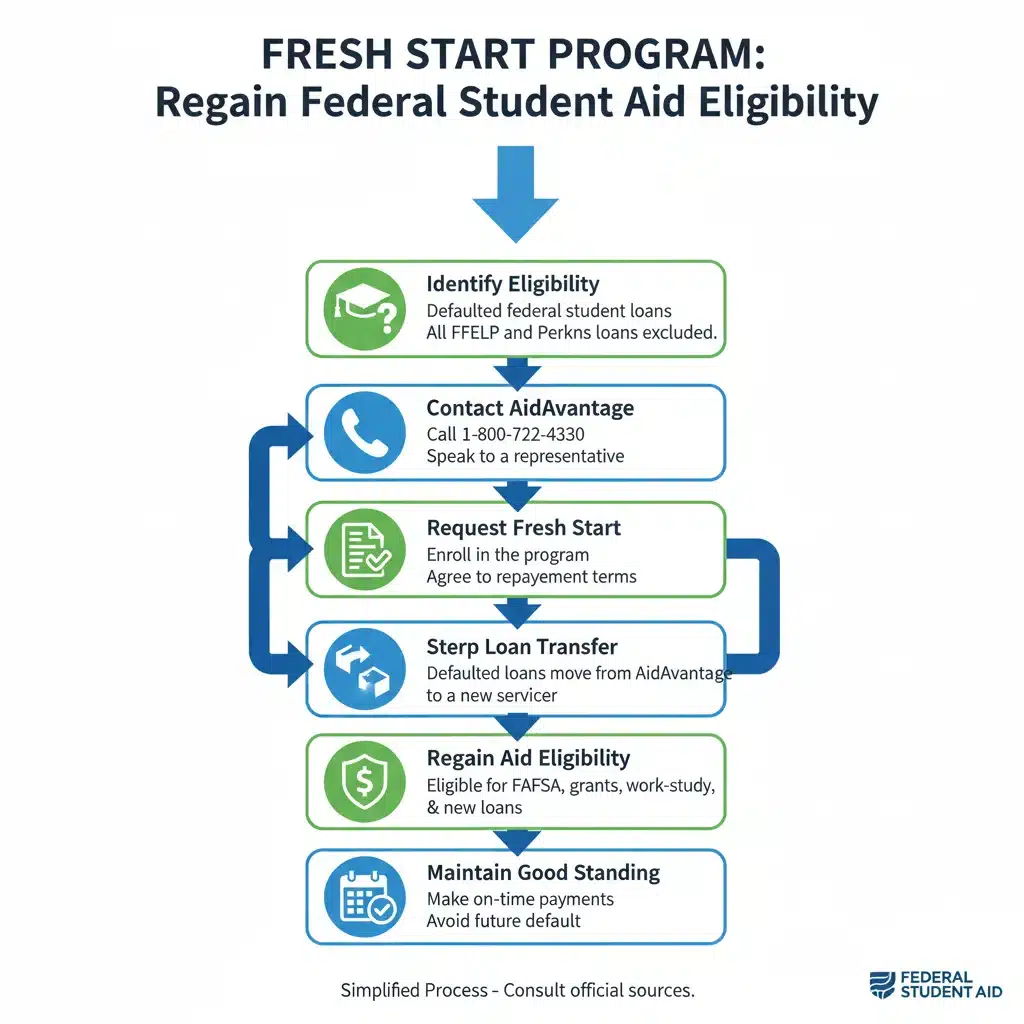

- Defaulted Federal Student Loans: Your loans must be federal student loans (e.g., Direct Loans, FFEL Program loans, Perkins Loans) that were in default prior to a specific date. This date has been a key component of the program’s eligibility window.

- Exclusion of Private Loans: The program does not apply to private student loans. Only federal loans are eligible.

- No Prior Rehabilitation or Consolidation During Specific Periods: In some instances, borrowers who recently rehabilitated or consolidated their loans might have different eligibility pathways or might not qualify if they did so during a specific timeframe.

If you are unsure whether your loans qualify, the best first step is to log into your StudentAid.gov account or contact your loan servicer directly. They can confirm the status of your loans and advise you on your eligibility for the Fresh Start Program.

The Path to Reclaiming Federal Student Aid Eligibility Within 3 Months

One of the most compelling aspects of the Fresh Start Program is its ability to quickly restore your eligibility for federal student aid. For many, this means the difference between continuing their education and being forced to postpone their academic goals. Here’s a breakdown of the steps involved in reclaiming your eligibility, often achievable within a three-month window:

Step 1: Identify Your Defaulted Loans and Loan Servicer

The very first step is to confirm which of your federal student loans are in default and who your current loan servicer is. You can do this by:

- Logging into your StudentAid.gov account using your FSA ID. This portal provides a comprehensive overview of all your federal student loans, their statuses, and the servicers assigned to them.

- Reviewing any correspondence you’ve received from collection agencies or the Department of Education.

Knowing your servicer is crucial, as they will be your primary point of contact for enrolling in the Fresh Start Program.

Step 2: Contact Your Loan Servicer or the Default Resolution Group

Once you’ve identified your defaulted loans and servicer, reach out to them directly. Inform them that you wish to utilize the Fresh Start Program to bring your loans out of default. If your loan has been transferred to a collection agency, you may need to contact the Default Resolution Group of the Department of Education:

- Default Resolution Group Contact: 1-800-621-3115 (for TTY, call 1-877-825-2368).

Clearly state your intent to enroll in the program. The representative will guide you through the next steps, which typically involve a simple verbal request or a short form.

Step 3: Agree to New Payment Terms (If Applicable)

While the initial Fresh Start period often involved an automatic return to good standing, future iterations or specific circumstances might require you to agree to new payment terms. This could involve enrolling in an Income-Driven Repayment (IDR) plan. IDR plans adjust your monthly payments based on your income and family size, making them more affordable. Even if not immediately required for Fresh Start, enrolling in an IDR plan is highly recommended to prevent future defaults and manage your debt sustainably.

Step 4: Confirm Your Loans Are Out of Default

After you’ve completed the necessary steps (contacting your servicer, making a request, and potentially agreeing to new terms), it’s crucial to confirm that your loans have been moved out of default status. This typically happens very quickly under the Fresh Start Program provisions, often within a few weeks. You can verify this by:

- Checking your StudentAid.gov account. The status of your loans should update from ‘defaulted’ to ‘current’ or ‘in good standing.’

- Contacting your loan servicer for a confirmation letter or email.

This confirmation is vital as it signifies your re-eligibility for federal student aid.

Step 5: Regain Eligibility for Federal Student Aid

Once your federal student loans are no longer in default through the Fresh Start Program, you immediately regain eligibility for federal student financial aid. This means you can:

- Apply for federal grants (like the Pell Grant).

- Access federal student loans (subsidized and unsubsidized).

- Enroll in work-study programs.

To access this aid, you will need to complete the Free Application for Federal Student Aid (FAFSA®) for the academic year you plan to attend. Ensure all your information is accurate and up-to-date. Your school’s financial aid office will then use your FAFSA information to determine your eligibility and package your aid.

The Three-Month Timeline: How It Works

The ability to reclaim eligibility within three months is a significant advantage of the Fresh Start Program. Here’s a typical breakdown:

- Week 1-2: Identify loans, contact servicer/Default Resolution Group, and make the request. This is often a quick process.

- Week 3-6: Loan status updates in the system. The Department of Education and servicers process the request, and your loan status changes from default to current.

- Week 7-12: Complete and submit your FAFSA. Once your loan status is updated, you can immediately file your FAFSA. The processing time for FAFSA and aid disbursement by your institution can vary, but the eligibility is restored quickly.

By acting promptly and following these steps, you can realistically be on your way to receiving federal student aid within a quarter of a year, paving the way for your educational aspirations.

Benefits Beyond Aid Eligibility: The Broader Impact of Fresh Start

The Fresh Start Program offers more than just renewed access to federal student aid; it provides a comprehensive reset for your financial health related to student loans. The benefits extend to several crucial areas:

Removal of Default Record from Credit Reports

Perhaps one of the most significant advantages is the removal of the default record from your credit history. This is different from traditional loan rehabilitation, which usually leaves a record of the default on your report even after rehabilitation. Under Fresh Start, the default status is erased, significantly improving your credit score and making it easier to secure other forms of credit in the future.

Cessation of Wage Garnishment and Tax Refund Offsets

Upon enrollment in the program, any ongoing wage garnishments or tax refund offsets are stopped. This immediately provides financial relief, allowing you to retain more of your earnings and tax refunds, which can be crucial for managing other living expenses.

Access to Income-Driven Repayment (IDR) Plans

Once your loans are out of default, you regain full access to all federal student loan benefits, including various Income-Driven Repayment (IDR) plans. These plans can significantly lower your monthly payments based on your income and family size, making your student loan debt much more manageable. They also offer the potential for loan forgiveness after a certain number of years of qualifying payments.

Eligibility for Deferment and Forbearance Options

Should you face future financial hardship, being in good standing means you can utilize deferment or forbearance options to temporarily pause or reduce your loan payments. These safety nets are unavailable when your loans are in default.

Opportunity for Loan Consolidation

With your loans out of default, you can explore federal loan consolidation. Consolidating your loans can simplify your repayment by combining multiple federal loans into a single new loan with one monthly payment. It can also open doors to different repayment plans and potentially lower your interest rate (though this is not guaranteed).

Avoiding Future Default: Strategies for Long-Term Success

While the Fresh Start Program offers a fantastic opportunity, the ultimate goal is to prevent future defaults. Here are proactive strategies to maintain good standing with your federal student loans:

Enroll in an Income-Driven Repayment (IDR) Plan

As mentioned, IDR plans are your best defense against default. They adjust your monthly payments to an affordable amount based on your discretionary income. If your income is low enough, your payment could be as little as $0 per month. Re-certify your income and family size annually to ensure your payments remain appropriate.

Understand Your Loan Servicer’s Role

Your loan servicer is your primary point of contact for all things related to your student loans. Don’t hesitate to reach out to them if you anticipate difficulty making payments, have questions about your balance, or need to explore repayment options. They are there to help you.

Utilize Deferment or Forbearance When Needed

If you experience temporary financial hardship (e.g., job loss, illness, economic downturn), deferment or forbearance can provide a temporary pause in payments. While interest may accrue during some of these periods, it’s a far better option than defaulting.

Create a Budget and Financial Plan

A clear understanding of your income and expenses is fundamental to managing debt. Create a realistic budget that prioritizes your student loan payments alongside other essential expenses. Look for areas where you can cut back to free up funds for debt repayment.

Consider Loan Consolidation (Strategic Use)

While consolidation doesn’t always lower your interest rate, it can simplify your repayment by combining multiple loans into one. This can make tracking payments easier and potentially open up new repayment plan options that better suit your financial situation.

Stay Informed About Policy Changes

Federal student loan policy is dynamic. Stay subscribed to updates from the Department of Education, follow reputable financial news sources, and regularly check StudentAid.gov. Being informed about new programs, changes to existing ones, or potential relief initiatives can help you make timely and beneficial decisions.

Common Misconceptions About the Fresh Start Program

Despite its significant benefits, there are several misconceptions surrounding the Fresh Start Program that can prevent eligible borrowers from taking advantage of it:

Misconception 1: It’s Too Complicated to Enroll

Reality: The enrollment process for the Fresh Start Program is remarkably straightforward, often requiring just a phone call to your loan servicer or the Default Resolution Group. It’s designed to be accessible, not complex.

Misconception 2: It Forgives All Your Debt

Reality: The program does not forgive your loan balance. Instead, it removes the default status and its associated negative consequences, allowing you to re-enter repayment in good standing. While it opens doors to IDR plans that can lead to forgiveness, the program itself is not a forgiveness program.

Misconception 3: You Can Only Use It Once

Reality: While the program is a temporary initiative, its specific rules regarding multiple uses can vary or be clarified with future updates. However, the primary goal is to get borrowers out of default once and provide tools to stay out of it.

Misconception 4: It Applies to All Student Loans

Reality: The Fresh Start Program is exclusively for eligible federal student loans. Private student loans are not included and have different default resolution processes.

Misconception 5: It’s Only for People Who Haven’t Made Any Payments

Reality: The program is for anyone whose federal student loans were in default prior to the specified cutoff date, regardless of whether they made some payments or none at all before defaulting. The key is the defaulted status.

The Broader Landscape of Student Loan Relief

The Fresh Start Program is an important piece of the larger puzzle of federal student loan relief. Beyond Fresh Start, the Department of Education offers several other avenues for borrowers struggling with student debt:

- Income-Driven Repayment (IDR) Plans: As discussed, these plans adjust your monthly payments based on your income and family size, with potential forgiveness after 20 or 25 years of payments.

- Public Service Loan Forgiveness (PSLF): For borrowers working in qualifying public service jobs, PSLF can forgive the remaining balance on Direct Loans after 120 qualifying monthly payments.

- Teacher Loan Forgiveness: Teachers in low-income schools may be eligible for forgiveness of up to $17,500 on their Direct Subsidized and Unsubsidized Loans.

- Total and Permanent Disability (TPD) Discharge: Borrowers who are totally and permanently disabled may be eligible to have their federal student loans discharged.

- Closed School Discharge: If your school closed while you were enrolled or shortly after you withdrew, you might be eligible for a discharge of your federal student loans.

Understanding these options, in conjunction with the Fresh Start Program, empowers you to make the best decisions for your financial future and educational goals.

Conclusion: A Fresh Start for Your Future

The Fresh Start Program represents a pivotal opportunity for millions of federal student loan borrowers. By offering a direct and efficient pathway out of default and a quick restoration of federal student aid eligibility, it empowers individuals to reset their financial standing and pursue their educational aspirations without the burden of past loan defaults. While specific updates for 2026 are still on the horizon, the core principles of the program—relief, rehabilitation, and renewed access—are expected to remain strong.

If you have defaulted federal student loans, do not delay. Take the proactive steps outlined in this guide: identify your loans, contact your servicer or the Default Resolution Group, and seize the opportunity to reclaim your financial health and educational future. The ability to regain federal student aid eligibility within three months is a powerful incentive to act now. Your fresh start is within reach.