Student Loan Scams 2026: Avoid Fraudulent Forgiveness Offers

Student Loan Scams 2026: Identifying and Avoiding Fraudulent Offers Promising Instant Forgiveness or 50% Debt Reduction

The landscape of student loan management is constantly evolving, and with it, unfortunately, the tactics of scammers. As we navigate 2026, the promise of student loan forgiveness and debt relief remains a beacon of hope for millions of borrowers. However, this hope often becomes a target for fraudulent schemes designed to exploit vulnerable individuals. Understanding how to identify and avoid student loan scams is more critical than ever. This comprehensive guide will equip you with the knowledge to protect yourself from predatory practices, safeguard your finances, and ensure you only engage with legitimate relief programs.

The Rising Tide of Student Loan Scams in 2026

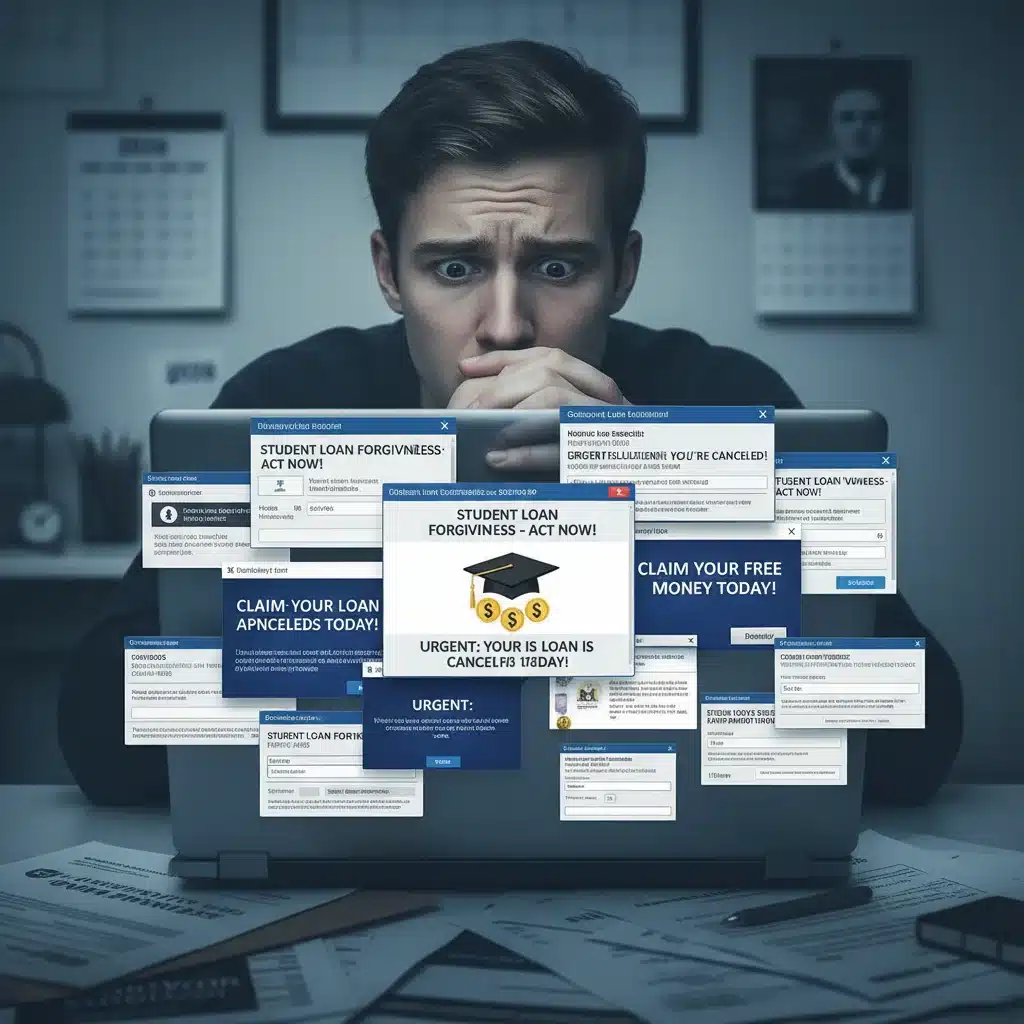

The past few years have seen unprecedented changes in student loan policies, including pauses on payments and discussions around widespread forgiveness. While these initiatives aim to help borrowers, they also create fertile ground for scammers. Fraudulent entities capitalize on the confusion and desperation of borrowers, offering enticing but ultimately fake solutions. These student loan scams often promise instant forgiveness, immediate debt reduction of 50% or more, or expedited access to legitimate programs – all for an upfront fee.

In 2026, scammers are becoming increasingly sophisticated. They leverage advanced communication technologies, including targeted social media ads, convincing email campaigns, and even personalized phone calls that mimic official government agencies or loan servicers. Their goal is simple: to extract personal financial information or upfront payments from unsuspecting individuals. Recognizing the signs of these scams is your first line of defense.

Why are Student Loan Scams So Prevalent?

The sheer volume of student loan debt in the United States, coupled with the complexity of repayment options and the constant evolution of federal programs, creates an environment ripe for fraud. Many borrowers feel overwhelmed and are desperate for relief. Scammers exploit this by:

- Creating a sense of urgency: They pressure borrowers to act immediately, claiming limited-time offers or imminent deadlines.

- Promising unrealistic results: Offers of instant forgiveness or massive debt reduction without eligibility checks are red flags.

- Mimicking official sources: They use names, logos, and website designs that closely resemble government agencies or reputable loan servicers.

- Exploiting confusion: The intricate details of student loan programs can be difficult to understand, making borrowers susceptible to misleading information.

Common Tactics Used in Student Loan Scams

Scammers employ a variety of tactics to ensnare borrowers. Being aware of these common approaches is crucial for protecting yourself from student loan scams.

1. Upfront Fees for “Forgiveness” or “Enrollment”

One of the most significant red flags is a request for an upfront fee to access loan forgiveness, consolidate debt, or enroll in a repayment program. Legitimate government programs and loan servicers never charge a fee to apply for or receive federal student loan benefits, including forgiveness, income-driven repayment plans, or consolidation. If someone asks you for money to process your application, it’s almost certainly a scam.

2. Guarantees of Instant or Total Forgiveness

No legitimate entity can guarantee instant or total student loan forgiveness. Federal forgiveness programs (like Public Service Loan Forgiveness or Teacher Loan Forgiveness) have strict eligibility requirements and often require years of qualifying payments or service. Any organization promising immediate, guaranteed forgiveness without verifying your eligibility is likely fraudulent. Be highly skeptical of claims like “Your debt will be wiped out today!” or “Guaranteed 50% debt reduction!”

3. Demands for Your Federal Student Aid (FSA) ID

Your FSA ID is your unique identifier for federal student aid websites and acts as your legal signature. Sharing it gives someone full access to your federal student aid accounts, allowing them to change your contact information, consolidate your loans, or even apply for new loans in your name. Never share your FSA ID with anyone. Legitimate loan servicers or the Department of Education will never ask for your FSA ID.

4. Pressure to Act Immediately

Scammers often create a false sense of urgency to bypass your critical thinking. They might claim that a special program is ending soon, or that you need to act within a specific, short timeframe to qualify for a benefit. This pressure is designed to prevent you from doing your research or seeking a second opinion. Legitimate offers typically provide ample time for consideration and application.

5. Misleading Communications (Emails, Texts, Calls)

Fraudulent communications often appear legitimate at first glance. They might use official-looking logos, government agency names (like the Department of Education or Federal Student Aid), or intimidating language to scare you into compliance. However, close inspection usually reveals inconsistencies:

- Generic Greetings: Instead of using your name, they might start with “Dear Borrower” or “To Whom It May Concern.”

- Grammatical Errors and Typos: Official communications are typically proofread meticulously.

- Suspicious Sender Addresses: Emails from non-governmental domains (e.g., Gmail, Yahoo, or domains that look similar but aren’t official .gov addresses).

- Links to Unofficial Websites: Always check the URL before clicking. Official government sites end in .gov.

- Unexpected Contact: If you haven’t initiated contact, be wary of unsolicited calls, texts, or emails, especially if they discuss your private financial information.

How to Protect Yourself from Student Loan Scams

Protecting yourself from student loan scams requires vigilance and adherence to best practices. Here are key steps you can take:

1. Know Your Loan Servicer

Your loan servicer is the company that handles your student loan billing and other services. You can find your servicer by logging into your account on StudentAid.gov. Any communication about your loans should come directly from your servicer or the Department of Education. If you receive contact from an unfamiliar company claiming to be your servicer, it’s a red flag.

2. Never Pay for Free Services

All federal student loan benefits, including applications for income-driven repayment plans, consolidation, and forgiveness programs, are free through the Department of Education and your loan servicer. You should never pay a third party for help with these processes. If you need assistance, contact your loan servicer directly or visit StudentAid.gov.

3. Protect Your FSA ID and Personal Information

Your FSA ID is your digital signature. Keep it private, just like your social security number or bank account details. Do not share it with anyone, especially not with companies claiming to help with your loans. Similarly, be cautious about sharing other sensitive personal or financial information with unsolicited contacts.

4. Verify All Communications

If you receive an unexpected call, email, or text about your student loans, do not respond directly. Instead, independently verify the claim. Look up the official contact information for your loan servicer or the Department of Education and reach out to them directly to inquire about the offer or message you received. Do not use contact information provided in the suspicious communication.

5. Be Wary of Unrealistic Promises

If an offer sounds too good to be true, it probably is. Instant forgiveness, guaranteed debt reduction, or promises to eliminate your loans without any effort on your part are hallmarks of student loan scams. Legitimate programs have eligibility criteria and often require a sustained period of qualifying payments or employment.

6. Understand Legitimate Student Loan Relief Programs

Familiarize yourself with the legitimate options available for federal student loan relief. These include:

- Income-Driven Repayment (IDR) Plans: These plans adjust your monthly payment based on your income and family size.

- Public Service Loan Forgiveness (PSLF): Forgives the remaining balance on Direct Loans after 120 qualifying monthly payments made under a qualifying repayment plan while working full-time for a qualifying employer.

- Teacher Loan Forgiveness: Forgives up to $17,500 for eligible teachers who work for five consecutive full academic years in certain low-income schools or educational service agencies.

- Total and Permanent Disability (TPD) Discharge: Forgives loans for borrowers who are totally and permanently disabled.

- Closed School Discharge: Forgives loans if your school closed while you were enrolled or shortly after you withdrew.

- Borrower Defense to Repayment: Forgives loans for borrowers who were defrauded by their school.

All applications for these programs can be found on StudentAid.gov or through your official loan servicer, and they are always free.

What to Do if You Suspect a Student Loan Scam

If you believe you have been targeted by or fallen victim to a student loan scam, immediate action is crucial:

1. Stop All Communication

Cease all contact with the suspected fraudulent entity. Do not provide any more information or make any further payments.

2. Report the Scam

- Federal Trade Commission (FTC): Report the scam to the FTC at ReportFraud.ftc.gov.

- Consumer Financial Protection Bureau (CFPB): File a complaint with the CFPB at consumerfinance.gov/complaint/.

- Department of Education: Contact the Federal Student Aid Information Center at 1-800-4-FEDAID (1-800-433-3243) or report fraud via their website.

- Your State Attorney General: File a complaint with your state’s Attorney General’s office.

- Your Loan Servicer: Inform your official student loan servicer about the fraudulent contact.

3. Monitor Your Financial Accounts and Credit Report

If you shared any personal or financial information, monitor your bank accounts, credit card statements, and credit report closely for any unauthorized activity. You can obtain a free copy of your credit report annually from AnnualCreditReport.com.

4. Change Passwords

If you shared your FSA ID or any other passwords with the scammers, change them immediately. Create strong, unique passwords for all your financial accounts.

Staying Informed in 2026 and Beyond

The best defense against student loan scams is a well-informed offense. Keep yourself updated on the latest student loan news and policy changes through official channels. Bookmark and regularly visit StudentAid.gov, which is the definitive source for federal student loan information. Sign up for email updates directly from the Department of Education to receive accurate information about any new programs or changes.

Be skeptical of any unsolicited offers, especially those that promise quick fixes or require upfront payments. Remember, legitimate help for your federal student loans is always free and accessible through your loan servicer or the Department of Education.

The Role of Media and Social Media

While social media can be a valuable tool for information sharing, it’s also a breeding ground for misinformation and scams. Be critical of posts and ads you see online, especially those promoting third-party student loan services. Always cross-reference any claims with official government sources before taking action.

Educating Others

If you encounter a student loan scam, share your experience with friends, family, and online communities. By raising awareness, you can help prevent others from falling victim to these predatory schemes. The more people who are educated about these tactics, the harder it becomes for scammers to succeed.

Conclusion: Your Vigilance is Your Best Defense Against Student Loan Scams

As we move further into 2026, the promise of student loan relief continues to be a significant topic for millions. While legitimate programs exist to help borrowers, the threat of student loan scams remains ever-present. These fraudulent schemes prey on hope and desperation, often promising instant forgiveness or substantial debt reduction in exchange for upfront fees or sensitive personal information.

Your best defense is vigilance. Always remember that legitimate federal student loan assistance is free, and official agencies will never demand your FSA ID or pressure you into immediate decisions. By staying informed, verifying all communications, and reporting suspicious activity, you can effectively protect yourself and your financial future from the deceptive tactics of student loan scammers. Empower yourself with knowledge, and ensure that your path to student loan relief is both legitimate and secure.