Income-Driven Repayment 2026: PAYE, IBR, ICR Compared for Student Loan Savings

Student loan debt remains a significant financial burden for millions of Americans. As we approach 2026, understanding the nuances of Income-Driven Repayment (IDR) plans becomes more critical than ever. These plans offer a lifeline, allowing borrowers to manage their federal student loan payments based on their income and family size, rather than their loan balance. For many, IDR plans are the key to avoiding default, achieving financial stability, and ultimately, securing loan forgiveness. This comprehensive guide will delve into the intricacies of the most prominent IDR plans – Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR) – providing a detailed comparison to help you determine which option offers the maximum savings for your specific situation in 2026.

The landscape of student loan repayment is constantly evolving. Regulatory changes, economic shifts, and personal circumstances all play a role in how borrowers navigate their debt. Staying informed about the latest provisions and understanding how each plan operates is paramount. Our focus, "Income-Driven Repayment 2026," aims to equip you with the knowledge needed to make informed decisions, potentially saving you thousands of dollars and years of repayment.

Understanding the Core Concept of Income-Driven Repayment (IDR)

Before we dive into the specifics of PAYE, IBR, and ICR, it’s essential to grasp the fundamental principle behind Income-Driven Repayment plans. IDR plans are designed to make federal student loan payments affordable by capping them at a percentage of your discretionary income. This means that if your income is low, your payments could be as little as $0 per month. After a certain period of payments (typically 20 or 25 years, depending on the plan and loan type), any remaining balance is forgiven. This forgiveness, however, may be subject to income tax, a crucial point often overlooked.

The primary goal of IDR plans is to prevent default and provide a pathway to repayment for borrowers who might otherwise struggle to meet their obligations under standard repayment plans. They offer flexibility, especially for those in lower-paying jobs, those experiencing unemployment, or those with large loan balances relative to their income. For "Income-Driven Repayment 2026" strategies, understanding this foundational concept is your first step.

Key Components of IDR Plans:

- Discretionary Income: This is the amount of your adjusted gross income (AGI) that exceeds a certain percentage of the federal poverty line for your family size and state of residence. The specific percentage varies by plan.

- Payment Cap: Your monthly payment is capped at a percentage of your discretionary income (e.g., 10%, 15%, or 20%).

- Annual Recertification: You must reapply annually, providing updated income and family size information, for your payments to be recalculated. Failure to recertify can lead to higher payments and capitalization of unpaid interest.

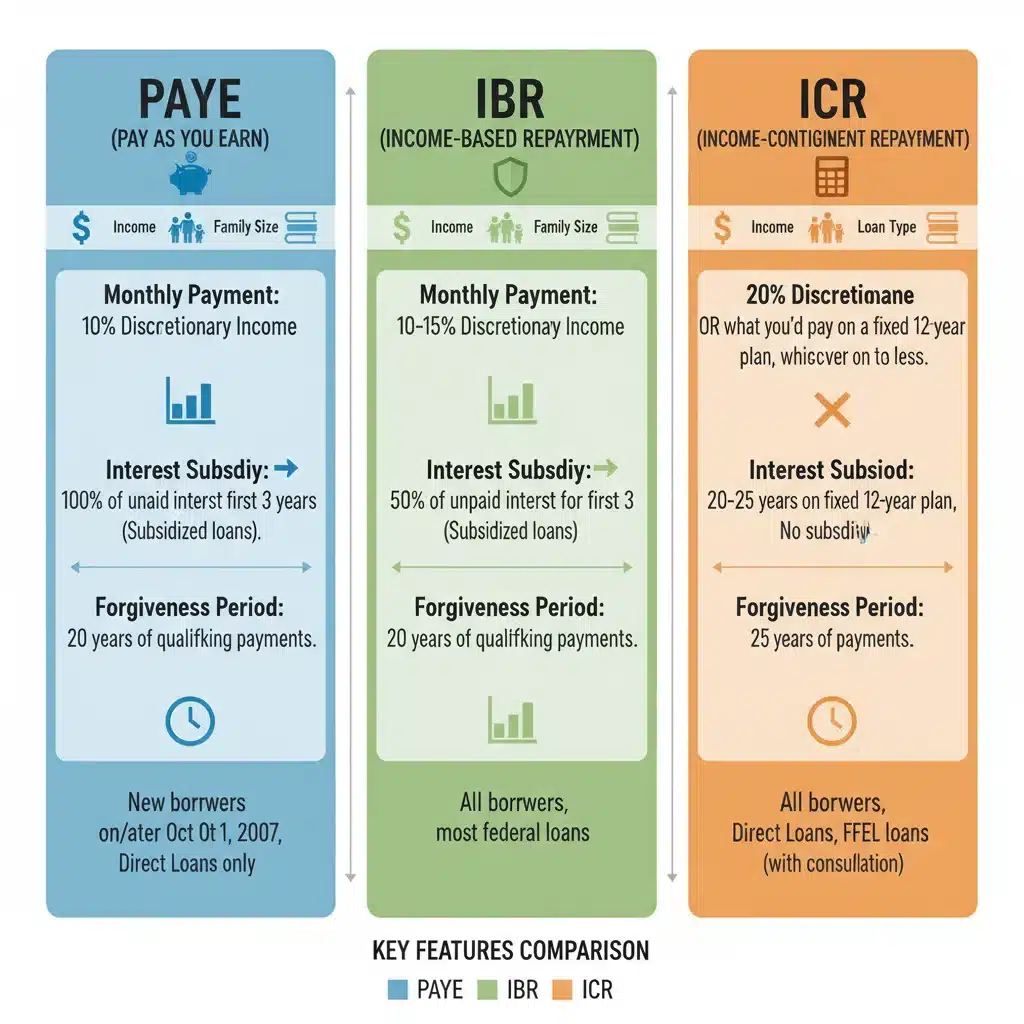

Deep Dive into Pay As You Earn (PAYE) for 2026

The Pay As You Earn (PAYE) repayment plan is often considered one of the most beneficial IDR options for eligible borrowers due to its lower payment cap and shorter forgiveness timeline for undergraduate loans. As we look at "Income-Driven Repayment 2026," PAYE continues to be a strong contender for many.

PAYE Eligibility Requirements:

To qualify for PAYE, you must meet specific criteria:

- New Borrower Requirement: You must be a "new borrower" as of October 1, 2007. This means you had no outstanding balance on a Direct Loan or FFEL Program loan when you received a Direct Loan or FFEL Program loan on or after October 1, 2007.

- Direct Loans Only: Only Direct Loans (Subsidized, Unsubsidized, PLUS loans made to students, and Direct Consolidation Loans that did not repay any FFEL Program loans) are eligible. FFEL loans must be consolidated into a Direct Consolidation Loan to qualify.

- Partial Financial Hardship (PFH): Your monthly payment under PAYE must be less than what you would pay under the Standard Repayment Plan with a 10-year repayment period. This is crucial; if your income is too high, you might not qualify.

How PAYE Payments are Calculated:

Under PAYE, your monthly payment is generally 10% of your discretionary income. Your discretionary income is the difference between your adjusted gross income (AGI) and 150% of the poverty guideline for your family size and state of residence. Your payment will never exceed what you would pay under the 10-year Standard Repayment Plan.

Loan Forgiveness under PAYE:

Any remaining loan balance is forgiven after 20 years of qualifying payments. This is a significant advantage over some other plans that require 25 years. However, the forgiven amount may be considered taxable income by the IRS, so it’s wise to plan for potential tax implications.

Benefits of PAYE:

- Lower Payments: Often results in the lowest monthly payments among IDR plans for many borrowers.

- Interest Subsidy: If your calculated payment doesn’t cover the interest on your subsidized loans, the government pays the remaining interest for up to three consecutive years.

- Shorter Forgiveness Period: 20 years for all loan types, making it appealing for those aiming for earlier debt relief.

Exploring Income-Based Repayment (IBR) in 2026

Income-Based Repayment (IBR) is one of the oldest and most widely available IDR plans. It offers flexibility for a broader range of borrowers compared to PAYE. When considering your "Income-Driven Repayment 2026" strategy, IBR is a plan you’ll definitely encounter.

IBR Eligibility Requirements:

IBR has more lenient eligibility criteria than PAYE:

- Eligible Loans: Direct Subsidized and Unsubsidized Loans, FFEL Subsidized and Unsubsidized Loans, Direct PLUS Loans made to students, FFEL PLUS Loans made to students, Direct Consolidation Loans, and FFEL Consolidation Loans. Parent PLUS loans are only eligible if consolidated into a Direct Consolidation Loan.

- Partial Financial Hardship (PFH): Similar to PAYE, your monthly payment under IBR must be less than what you would pay under the Standard Repayment Plan with a 10-year repayment period.

How IBR Payments are Calculated:

The payment calculation for IBR depends on when you took out your loans:

- New Borrowers (on or after July 1, 2014): Your monthly payment is 10% of your discretionary income, capped at the amount you would pay under the 10-year Standard Repayment Plan. Discretionary income is defined as AGI minus 150% of the poverty guideline.

- Older Borrowers (before July 1, 2014): Your monthly payment is 15% of your discretionary income, capped at the amount you would pay under the 10-year Standard Repayment Plan. Discretionary income is defined as AGI minus 150% of the poverty guideline.

Loan Forgiveness under IBR:

Any remaining balance is forgiven after 20 years of qualifying payments if you are a new borrower (on or after July 1, 2014) and after 25 years for older borrowers. Similar to PAYE, the forgiven amount may be taxable.

Benefits of IBR:

- Broad Eligibility: Available to a wider range of federal student loan borrowers, including those with older FFEL loans.

- Interest Subsidy: For subsidized loans, the government pays up to three years of unpaid interest if your payment doesn’t cover it.

Dissecting Income-Contingent Repayment (ICR) for 2026

The Income-Contingent Repayment (ICR) plan is the oldest IDR plan and serves as a fallback option for some borrowers who don’t qualify for other plans, particularly Parent PLUS borrowers who consolidate their loans. For "Income-Driven Repayment 2026," ICR might be less common for direct student loans but remains vital for specific situations.

ICR Eligibility Requirements:

- Eligible Loans: Direct Subsidized and Unsubsidized Loans, Direct PLUS Loans made to students, and Direct Consolidation Loans. Parent PLUS loans become eligible if they are first consolidated into a Direct Consolidation Loan. FFEL loans must also be consolidated.

- No Partial Financial Hardship Required: Unlike PAYE and IBR, you do not need to demonstrate a partial financial hardship to qualify for ICR. This makes it accessible to borrowers with higher incomes who still want the flexibility of an IDR plan.

How ICR Payments are Calculated:

ICR payments are calculated as the lesser of:

- 20% of your discretionary income (defined as AGI minus 100% of the poverty guideline for your family size).

- What you would pay on a fixed repayment plan over 12 years, adjusted according to your income.

The calculation for discretionary income in ICR is less generous (100% of the poverty line vs. 150% for PAYE/IBR), often resulting in higher payments than other IDR plans for the same income level.

Loan Forgiveness under ICR:

Any remaining loan balance is forgiven after 25 years of qualifying payments. As with other IDR plans, this forgiven amount may be taxable income.

Benefits of ICR:

- Broadest Eligibility: The only IDR plan available to Parent PLUS borrowers (after consolidation) and does not require a partial financial hardship.

- Simpler Qualification: No PFH test means it’s easier to qualify for if other IDR plans are out of reach.

Comparing PAYE, IBR, and ICR: Which Offers Maximum Savings in 2026?

Choosing the right IDR plan is not a one-size-fits-all decision. The optimal plan for you depends on several factors, including your income, family size, loan types, and when you took out your loans. For "Income-Driven Repayment 2026," a direct comparison is essential to identify the path to maximum savings.

| Feature | PAYE | IBR (New Borrowers) | IBR (Older Borrowers) | ICR |

|---|---|---|---|---|

| Eligible Loans | Direct Loans (Student) | Direct & FFEL (Student, Parent PLUS via Consolidation) | Direct & FFEL (Student, Parent PLUS via Consolidation) | Direct Loans (Student, Parent PLUS via Consolidation) |

| New Borrower Req. | Yes (after Oct 1, 2007) | Yes (after July 1, 2014) | No | No |

| PFH Required | Yes | Yes | Yes | No |

| Payment % of Discretionary Income | 10% | 10% | 15% | 20% (or 12-year fixed, whichever is less) |

| Discretionary Income Definition | AGI – 150% Poverty Line | AGI – 150% Poverty Line | AGI – 150% Poverty Line | AGI – 100% Poverty Line |

| Payment Cap | 10-year Standard Payment | 10-year Standard Payment | 10-year Standard Payment | No (but formula limits it) |

| Forgiveness Period | 20 years | 20 years | 25 years | 25 years |

| Interest Subsidy | Yes (Subsidized loans, 3 yrs) | Yes (Subsidized loans, 3 yrs) | Yes (Subsidized loans, 3 yrs) | No |

When PAYE is Your Best Bet:

PAYE is generally the most advantageous for borrowers who:

- Are "new borrowers" (as defined above).

- Have a relatively low income compared to their debt, qualifying them for a partial financial hardship.

- Want the lowest possible monthly payments and a shorter forgiveness period (20 years).

When IBR (New Borrowers) is Ideal:

If you don’t qualify for PAYE due to the "new borrower" requirement but took out your first loans after July 1, 2014, IBR for new borrowers offers similar benefits with a 10% payment cap and 20-year forgiveness. It’s a strong alternative to PAYE if you meet its specific criteria.

When IBR (Older Borrowers) Makes Sense:

For those with older loans (before July 1, 2014), IBR is often the best option, especially if you have FFEL loans that were not consolidated early on. While the payment percentage is higher (15%) and the forgiveness period longer (25 years), it still provides significant relief compared to standard plans.

When ICR is the Right Choice:

ICR is primarily suited for:

- Parent PLUS loan borrowers who have consolidated their loans into a Direct Consolidation Loan. This is often their only IDR option.

- Borrowers who don’t qualify for PAYE or IBR due to not having a partial financial hardship, but still desire income-based payments.

Crucial Considerations for "Income-Driven Repayment 2026"

Beyond the direct comparison, several factors can influence your choice and the overall effectiveness of your IDR plan.

The Revised Pay As You Earn (REPAYE) Plan and SAVE Plan:

It’s important to note the existence of the Revised Pay As You Earn (REPAYE) plan, which was rebranded as the Saving on a Valuable Education (SAVE) Plan in 2023. While not one of the three primary plans discussed in detail here, SAVE has become the most generous IDR plan for many borrowers. SAVE offers:

- Lower Payments: Payments are 10% of discretionary income for undergraduate loans, and a weighted average for those with both undergraduate and graduate loans. Beginning July 1, 2024, payments for undergraduate loans will drop to 5% of discretionary income.

- More Generous Discretionary Income Calculation: Discretionary income is calculated as AGI minus 225% of the poverty guideline, meaning more of your income is protected.

- Full Interest Subsidy: Any interest not covered by your monthly payment is fully subsidized, preventing your loan balance from growing due to unpaid interest. This is a massive benefit.

- Shorter Forgiveness: 10-20 years for original loan balances of $12,000 or less, increasing by one year for every additional $1,000 borrowed, up to 20 or 25 years.

- Broader Eligibility: Available to all Direct Loan borrowers, regardless of when they took out their loans or if they have a partial financial hardship.

For many borrowers, especially those with undergraduate loans and lower incomes, the SAVE Plan (formerly REPAYE) will offer the maximum savings and should be your first consideration for "Income-Driven Repayment 2026." However, if you have a high income and a large loan balance, the payment cap on PAYE or IBR might be more beneficial as SAVE does not have a payment cap based on the 10-year Standard Repayment Plan.

Public Service Loan Forgiveness (PSLF):

If you work for a government agency or a qualifying non-profit organization, Public Service Loan Forgiveness (PSLF) can be a game-changer. Under PSLF, any remaining balance on your Direct Loans is forgiven after 120 qualifying monthly payments (10 years) while working full-time for a qualifying employer. Payments made under any IDR plan (including PAYE, IBR, ICR, and SAVE) count towards PSLF. If you are pursuing PSLF, choosing the IDR plan that results in the lowest monthly payment will maximize the amount forgiven.

Taxability of Forgiven Debt:

As mentioned, loan forgiveness under IDR plans (excluding PSLF) is generally considered taxable income by the IRS. This is a critical point for "Income-Driven Repayment 2026" planning. While the American Rescue Plan Act of 2021 made IDR forgiveness tax-free through December 31, 2025, this provision is set to expire. Unless extended, borrowers receiving IDR forgiveness in 2026 and beyond will likely face a significant tax bill. It’s crucial to consult with a tax professional and potentially save for this future liability.

Annual Recertification:

This cannot be stressed enough: you MUST recertify your income and family size annually. Missing the deadline or failing to provide documentation can lead to your payments reverting to the 10-year Standard Repayment amount, and any unpaid interest capitalizing (added to your principal balance), increasing your total debt. Stay organized and set reminders for your recertification date.

Marriage and Income:

How marriage impacts your IDR payments varies by plan. For PAYE and IBR, if you file taxes separately, your spouse’s income is generally not included in your discretionary income calculation. However, for SAVE (REPAYE) and ICR, your spouse’s income is always considered, regardless of filing status. This can significantly impact your monthly payment, so it’s a vital consideration for married borrowers when planning for "Income-Driven Repayment 2026."

How to Apply for or Switch IDR Plans

Applying for an IDR plan or switching between them is a straightforward process:

- Gather Your Documents: You’ll need your federal student aid ID, your most recent tax return (or alternative documentation of income if your income has changed significantly), and information about your family size.

- Contact Your Loan Servicer: Your loan servicer is your primary point of contact for all repayment-related inquiries. They can help you understand your options and provide the necessary forms.

- Use StudentAid.gov: The Federal Student Aid website (StudentAid.gov) offers an online application for IDR plans. It also has a Repayment Estimator tool that can help you compare payments under various plans. This tool is invaluable for projecting your "Income-Driven Repayment 2026" scenario.

- Submit Your Application: Complete the Income-Driven Repayment Plan Request form and submit it to your loan servicer.

Final Thoughts on Maximizing Savings with "Income-Driven Repayment 2026"

Navigating student loan repayment can feel overwhelming, but understanding Income-Driven Repayment plans is a powerful tool for taking control of your financial future. As we look towards "Income-Driven Repayment 2026," remember that the best plan for you is highly individualized.

For most eligible borrowers, the SAVE Plan (formerly REPAYE) will offer the lowest monthly payments and the greatest interest benefits, potentially leading to significant savings and faster forgiveness. However, PAYE remains an excellent option for those who qualify due to its payment cap and 20-year forgiveness. IBR provides a wider net of eligibility, particularly for older loans, and ICR serves as a crucial option for Parent PLUS borrowers and those who don’t meet other hardship requirements.

Do not hesitate to use the resources available to you, including the Repayment Estimator on StudentAid.gov and direct communication with your loan servicer. Consider seeking advice from a qualified financial advisor, especially if your situation is complex or if you’re weighing the tax implications of forgiveness. By actively managing your student loans and choosing the most appropriate IDR plan, you can significantly reduce your financial stress and work towards a debt-free future. Your proactive approach to "Income-Driven Repayment 2026" will truly pay off.