SAVE Plan 2026: Maximize Reduced Payments & 10-Year Forgiveness

The landscape of student loan repayment is constantly evolving, and for federal student loan borrowers, understanding these changes is paramount to financial well-being. Among the most significant developments is the SAVE Plan (Saving on a Valuable Education), which is set to fully implement its most impactful features in 2026. This plan represents a substantial shift in how millions of Americans will manage their student debt, offering unprecedented opportunities for reduced payments and accelerated loan forgiveness.

For many, the promise of a more affordable monthly payment and a clearer path to forgiveness is a beacon of hope. However, navigating the intricacies of the SAVE Plan, especially as it fully rolls out in 2026, requires careful attention to detail. This comprehensive guide will delve deep into the SAVE Plan, focusing on how you can maximize your reduced payments and, crucially, understand the 10-year forgiveness timeline that is becoming a reality for a significant portion of borrowers.

We’ll explore the core mechanics of the plan, who stands to benefit the most, and what steps you need to take to ensure you’re positioned to take full advantage of its provisions. Whether you’re currently enrolled, considering enrolling, or simply trying to make sense of the new student loan environment, this article will provide you with the essential information you need to make informed decisions about your financial future.

Understanding the SAVE Plan: A New Era for Student Loan Repayment

The SAVE Plan is an income-driven repayment (IDR) plan designed to make student loan payments more affordable and to provide a faster route to loan forgiveness. It replaces the Revised Pay As You Earn (REPAYE) plan, building upon its framework while introducing several borrower-friendly enhancements. The core philosophy behind SAVE is to ensure that borrowers are not burdened by payments that exceed their financial capacity, thereby reducing defaults and providing a clearer path out of debt.

Unlike traditional repayment plans that are fixed, IDR plans like SAVE adjust your monthly payment based on your income and family size. This flexibility is particularly beneficial for those with lower incomes relative to their student loan debt, as it prevents payments from becoming an insurmountable obstacle to other financial goals, such as saving for a home or retirement.

The SAVE Plan was initially introduced in the summer of 2023, with some of its features taking effect immediately. However, the most significant changes, particularly those related to the calculation of discretionary income and the accelerated forgiveness timeline, are slated for full implementation in July 2024 and subsequently in 2026. This phased rollout means that borrowers need to stay informed about the specific dates when certain provisions become active.

One of the most impactful aspects of the SAVE Plan is its promise of not allowing unpaid interest to capitalize, meaning your loan balance won’t grow as long as you’re making your required monthly payments, even if those payments are $0. This is a game-changer for many borrowers who have seen their loan balances swell despite making consistent payments under previous IDR plans.

Moreover, the SAVE Plan offers a faster path to forgiveness for certain borrowers, a feature that will be fully realized by 2026. This accelerated forgiveness is a direct response to the long repayment periods often associated with IDR plans, which could sometimes feel like a never-ending cycle of debt. With SAVE, the finish line is closer for many, providing a tangible end to their student loan obligations.

It’s important to distinguish the SAVE Plan from other student loan initiatives. While there have been discussions and actions regarding broad student loan forgiveness, the SAVE Plan is a specific IDR program with its own set of rules and eligibility criteria. It focuses on making repayment manageable and offering forgiveness after a defined period of qualifying payments, rather than a one-time blanket forgiveness.

Key Changes Coming in 2026: What Borrowers Need to Know

While some elements of the SAVE Plan are already in effect, 2026 marks the full implementation of its most transformative provisions. These changes are designed to further reduce the financial burden on borrowers and accelerate their journey to forgiveness. Understanding these upcoming changes is crucial for strategic financial planning.

Reduced Discretionary Income Calculation

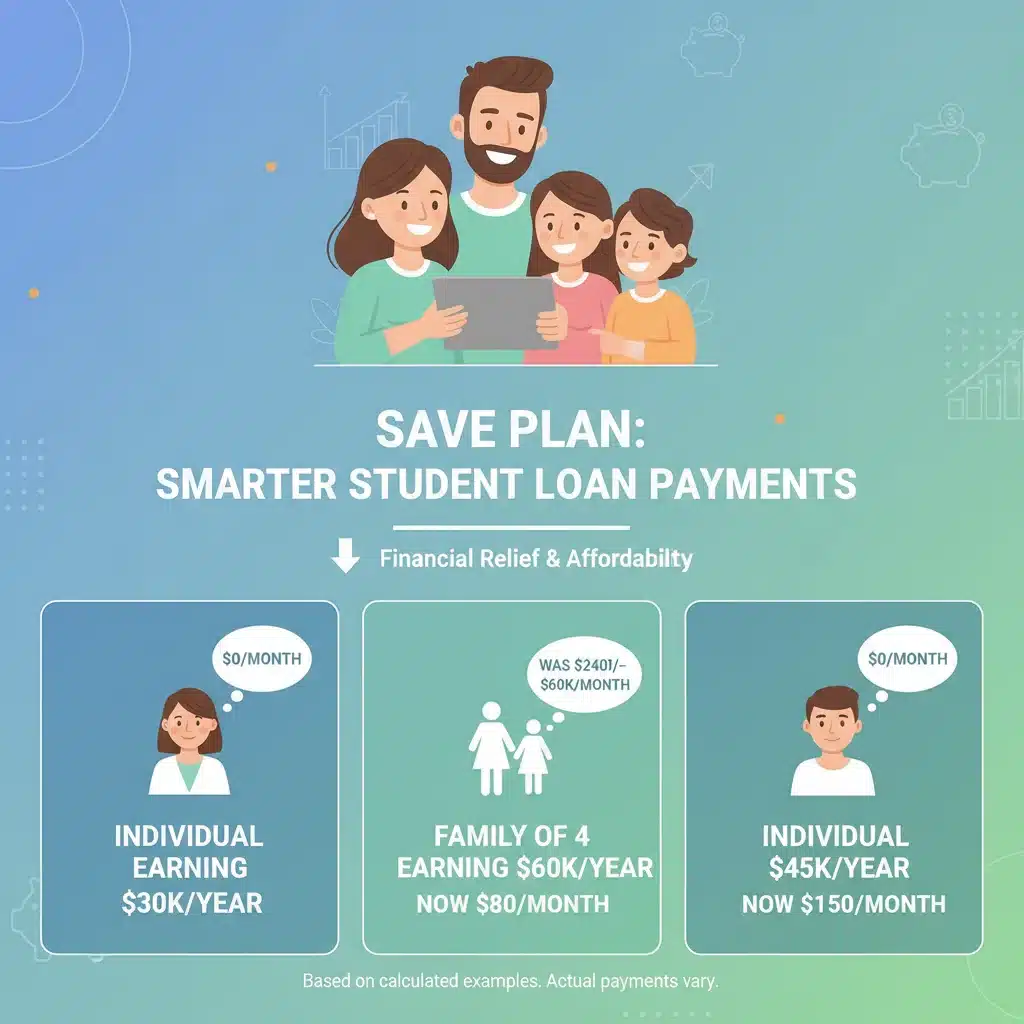

One of the most significant changes arriving in 2026 (with some aspects beginning in July 2024) pertains to how your discretionary income is calculated. Under the current and previous IDR plans, discretionary income was generally defined as the difference between your adjusted gross income (AGI) and 150% of the federal poverty guideline for your family size. The SAVE Plan significantly improves upon this by increasing the income shielded from payments.

- For undergraduate loans: Your discretionary income will be calculated as the difference between your AGI and 225% of the federal poverty guideline. This means a much larger portion of your income is protected, leading to lower monthly payments for most borrowers with undergraduate loans.

- For graduate loans: Your discretionary income will be calculated as the difference between your AGI and 225% of the federal poverty guideline, but your payment will be set at 10% of that discretionary income (compared to 5% for undergraduate loans).

This adjustment is critical because it directly impacts your monthly payment amount. By shielding more of your income, the SAVE Plan ensures that your student loan payment is a smaller percentage of your actual disposable income, making it more affordable and sustainable. For many, this could mean monthly payments that are substantially lower than what they would pay under other IDR plans or standard repayment plans.

Lower Payment Percentages (Effective July 2024, fully realized by 2026)

Another major change is the reduction in the percentage of discretionary income used to calculate monthly payments. Starting in July 2024, borrowers with only undergraduate loans will see their payments drop from 10% of their discretionary income to 5%. Borrowers with a mix of undergraduate and graduate loans will have a weighted average applied, ensuring fairness across different loan types.

This reduction, combined with the expanded definition of protected income, creates a powerful one-two punch for affordability. It’s designed to provide substantial relief, especially for recent graduates or those in lower-paying careers who are struggling to manage their debt.

No Accrual of Unpaid Interest (Already in Effect)

While not strictly a 2026 change, the no accrual of unpaid interest feature is a cornerstone of the SAVE Plan and essential to understand in the context of its overall benefits. Under previous IDR plans, if your monthly payment was not enough to cover the interest accruing on your loans, the unpaid interest would be added to your principal balance (capitalized). This could lead to your loan balance growing even as you made payments, a phenomenon known as negative amortization.

The SAVE Plan eliminates this problem. As long as you make your required monthly payment, even if it’s as low as $0, your loan balance will not grow due to unpaid interest. The Department of Education will cover any interest not covered by your payment. This feature prevents the disheartening experience of seeing your debt increase despite your best efforts, making the path to forgiveness more straightforward and less psychologically taxing.

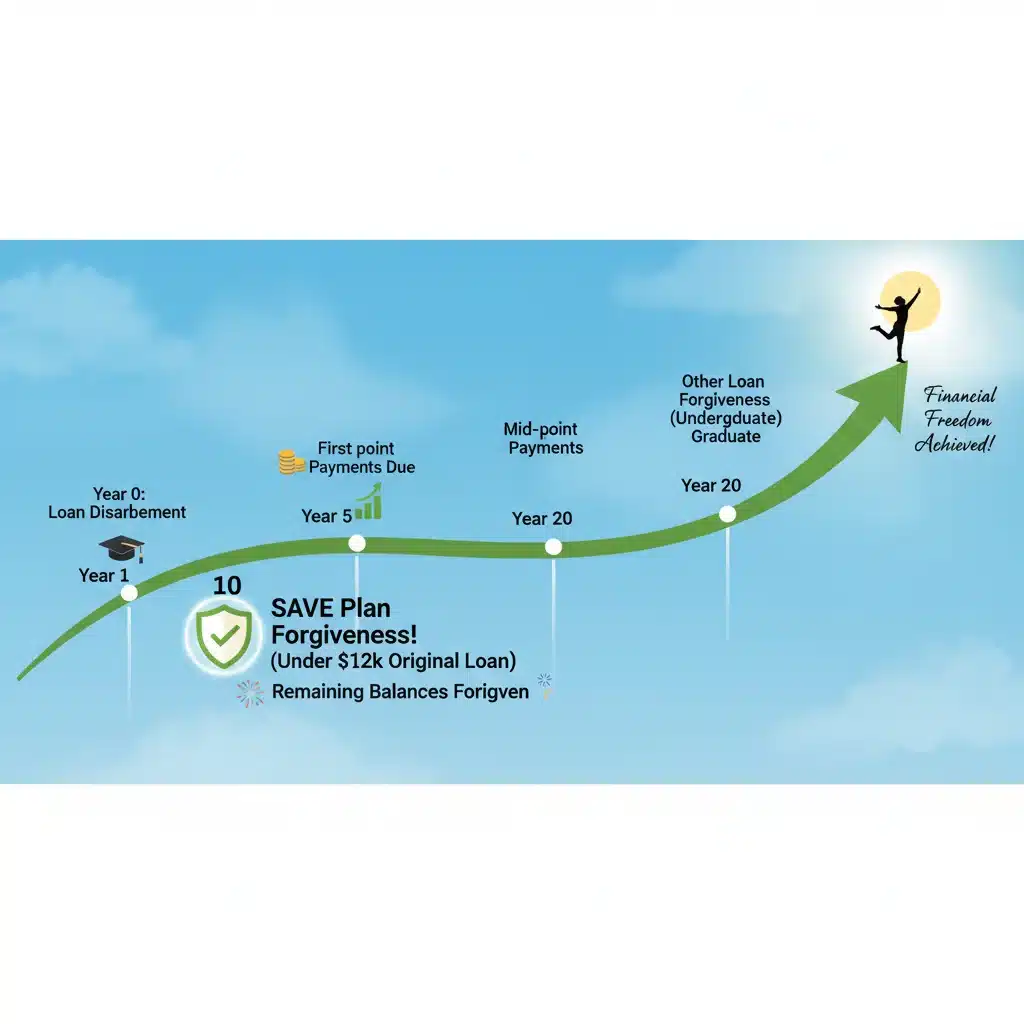

The 10-Year Forgiveness Timeline: A Game Changer

Perhaps the most exciting and anticipated feature of the SAVE Plan, fully taking effect by 2026, is the accelerated forgiveness timeline for certain borrowers. This provision drastically reduces the time it takes to achieve loan forgiveness, particularly for those with smaller original loan balances.

Who Qualifies for 10-Year Forgiveness?

Under the SAVE Plan, borrowers whose original principal loan balances were $12,000 or less will be eligible for forgiveness after just 10 years of qualifying payments. For every additional $1,000 borrowed above $12,000, the forgiveness timeline increases by one year, up to a maximum of 20 years for undergraduate loans and 25 years for graduate loans.

This means that if you initially borrowed $12,000 or less, you could see your federal student loans forgiven after a decade of making payments, potentially saving you thousands of dollars and years of repayment. This is a stark contrast to the previous IDR plans, which typically required 20 or 25 years of payments for forgiveness, regardless of the original loan amount.

The calculation of the original principal balance includes both your initial loan amount and any accrued interest that capitalized before you began repayment on an IDR plan. It’s crucial to understand your original loan amount to accurately determine your forgiveness timeline under SAVE.

The Impact of Accelerated Forgiveness

The 10-year forgiveness timeline has profound implications for borrowers. It provides a much clearer and more attainable goal, allowing individuals to plan their financial futures with greater certainty. For those with lower loan balances, the prospect of being debt-free in a decade can be life-changing, freeing up resources for other investments, family planning, or career changes.

Moreover, this feature incentivizes enrollment in the SAVE Plan, as it offers a tangible benefit that was not available under previous IDR plans. It moves beyond simply managing payments to actively working towards a defined endpoint of debt relief.

Counting Qualifying Payments

It’s important to note that the 10-year (or longer) forgiveness timeline counts qualifying payments. A qualifying payment is generally a monthly payment made under an IDR plan, or any month in a repayment status, even if your payment was $0 due to low income. This also includes periods of economic hardship deferment, certain forbearances, and military service.

The Department of Education is conducting a one-time adjustment to count past periods of repayment, deferment, and forbearance towards IDR forgiveness, including for the SAVE Plan. This adjustment aims to correct past administrative issues and ensure that borrowers receive credit for time spent in repayment that should have counted towards forgiveness. This means many borrowers will find themselves closer to forgiveness than they initially thought, even before the full SAVE Plan implementation in 2026.

Maximizing Your Reduced Payments Under SAVE

Simply enrolling in the SAVE Plan is the first step; maximizing its benefits requires a strategic approach to your finances and understanding of the plan’s rules. Here’s how to ensure you’re getting the most out of your reduced payments.

Enroll Early and Stay Enrolled

If you’re not already on the SAVE Plan, consider enrolling as soon as possible. While some of the most beneficial features arrive in 2026, the immediate benefits, such as the interest subsidy and initial payment reductions, can provide significant relief now. The sooner you enroll, the sooner your qualifying payments begin counting towards forgiveness.

The application process is straightforward and can be completed through the Federal Student Aid website (studentaid.gov). You’ll need to provide information about your income and family size.

Recertify Your Income Annually

To keep your payments accurate and reflective of your current financial situation, you must recertify your income and family size annually. Failing to recertify can lead to your payments reverting to a higher amount (what you would pay under a standard 10-year repayment plan), and any unpaid interest may capitalize. The Department of Education will typically send reminders, but it’s ultimately your responsibility to track this deadline.

If your income decreases, recertifying promptly can lead to an immediate reduction in your monthly payment. Conversely, if your income increases significantly, your payments may go up, but they will still be capped at an affordable percentage of your discretionary income.

Understand Your Household Income and Family Size

Your monthly payment is heavily influenced by your reported income and family size. Ensure these details are accurate during your application and annual recertification. For married borrowers, whether you file taxes jointly or separately can impact your discretionary income calculation. Filing separately often allows only your individual income to be considered, potentially leading to lower payments, especially if your spouse has a higher income and does not have federal student loans.

Your family size includes yourself, your spouse (if filing jointly), and any children or other dependents you support. An increase in family size can lower your discretionary income and, consequently, your monthly payment.

Consider Your Tax Filing Status

As mentioned, your tax filing status can significantly impact your SAVE Plan payments. If you are married, filing separately (MFS) may exclude your spouse’s income from your discretionary income calculation, potentially leading to a lower monthly payment. However, MFS can have other tax implications, such as losing certain tax credits or deductions. It’s advisable to consult with a tax professional to determine the best filing strategy for your specific situation, weighing the student loan payment benefits against potential tax costs.

Monitor Your Loan Servicer Communications

Your loan servicer is your primary point of contact for managing your loans under the SAVE Plan. Pay close attention to all communications from them, as they will provide important updates, recertification reminders, and information about your payment status. If you have questions or concerns, reach out to your servicer directly.

Eligibility and Enrollment for the SAVE Plan

To take advantage of the SAVE Plan, you must meet certain eligibility requirements and complete the enrollment process. Understanding these steps is crucial for accessing the plan’s benefits.

Who is Eligible?

The SAVE Plan is available to borrowers with eligible federal student loans. This primarily includes:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans made to students

- Direct Consolidation Loans (that did not repay Parent PLUS Loans)

Federal Family Education Loan (FFEL) Program loans and Perkins Loans are generally not directly eligible unless they are consolidated into a Direct Consolidation Loan. However, if you consolidate these loans, they will then become eligible for the SAVE Plan. Parent PLUS Loans are not eligible for the SAVE Plan, even if consolidated, unless they are included in a Direct Consolidation Loan that only contains Parent PLUS loans, which then can be repaid under the Income-Contingent Repayment (ICR) plan, and then potentially benefit from some IDR adjustments.

It’s important to confirm the eligibility of your specific loan types. You can check your loan details by logging into your account on studentaid.gov.

How to Enroll

Enrolling in the SAVE Plan is a straightforward process:

- Visit StudentAid.gov: Navigate to the income-driven repayment (IDR) plan application.

- Choose the SAVE Plan: Select the SAVE Plan as your preferred repayment option. If you are currently on the REPAYE Plan, you will automatically be transferred to the SAVE Plan.

- Provide Income and Family Size Information: You will need to provide documentation of your income (e.g., tax return, pay stubs) and certify your family size. You can often link to the IRS to automatically retrieve your tax information, simplifying the process.

- Review and Submit: Carefully review all the information before submitting your application.

- Monitor Your Account: After submission, keep an eye on your loan servicer’s communications for confirmation of your enrollment and your new payment amount.

The application process usually takes a few minutes, but processing times can vary. It’s advisable to apply well before your next payment due date to ensure your new payment amount is in effect.

Potential Pitfalls and Considerations

While the SAVE Plan offers significant advantages, it’s essential to be aware of potential pitfalls and considerations to ensure it’s the right choice for your financial situation.

Tax Bomb on Forgiveness

Currently, under federal law, any loan amount forgiven under an IDR plan, including SAVE, is considered taxable income by the IRS. This means that when your loans are forgiven after 10, 20, or 25 years, you could face a substantial tax bill. However, there’s a temporary provision in the American Rescue Plan Act of 2021 that makes IDR forgiveness tax-free at the federal level through December 31, 2025. What happens after this date is uncertain. Borrowers should monitor legislative developments or consult with a tax advisor as they approach their forgiveness date, especially if it falls after 2025.

Complexity and Administrative Burden

While simplified, IDR plans still require annual recertification of income and family size. This administrative task, if overlooked, can lead to higher payments or accrued interest capitalization. It’s crucial to stay organized and proactive in managing your SAVE Plan enrollment.

Impact on Future Borrowing

While the SAVE Plan helps manage current debt, having a significant outstanding student loan balance, even with low payments, can sometimes impact your ability to qualify for other loans, such as mortgages or car loans. Lenders consider your debt-to-income ratio, and student loan payments, even if low, are part of that calculation.

Not for Everyone

The SAVE Plan is ideal for borrowers with high debt-to-income ratios or those seeking the lowest possible monthly payments and a path to forgiveness. However, if you have a relatively low loan balance and a high income, a standard repayment plan might allow you to pay off your loans faster and with less overall interest, avoiding the potential tax bomb on forgiveness.

Comparison with Other IDR Plans

For context, it’s helpful to briefly compare the SAVE Plan with other existing Income-Driven Repayment plans, as it highlights why SAVE is often the superior choice for many borrowers.

- Income-Based Repayment (IBR): Payments are generally 10% or 15% of discretionary income, with forgiveness after 20 or 25 years. The definition of discretionary income is less generous than SAVE (150% of poverty line).

- Pay As You Earn (PAYE): Payments are 10% of discretionary income (150% of poverty line), with forgiveness after 20 years. Eligibility is restricted to new borrowers on or after October 1, 2007, and must have received a disbursement of a Direct Loan on or after October 1, 2011.

- Income-Contingent Repayment (ICR): Payments are either 20% of discretionary income (100% of poverty line) or what you’d pay on a fixed 12-year plan, whichever is less. Forgiveness after 25 years. This is generally the least generous IDR plan and is often the only option for Parent PLUS loan borrowers who consolidate.

The SAVE Plan generally offers the lowest monthly payments due to its expanded definition of protected income and lower payment percentages for undergraduate loans. Its interest subsidy and accelerated forgiveness for lower balances further solidify its position as the most beneficial IDR plan for a vast majority of eligible federal student loan borrowers.

Looking Ahead to 2026 and Beyond

The full implementation of the SAVE Plan in 2026 marks a pivotal moment for federal student loan borrowers. As the new provisions take full effect, millions will experience more manageable monthly payments and a clearer, faster path to loan forgiveness. This represents a significant step towards addressing the national student debt crisis and providing much-needed relief to individuals and families.

However, the student loan landscape is subject to change, influenced by political shifts, economic conditions, and legislative actions. It’s imperative for borrowers to remain engaged, stay informed through official sources like StudentAid.gov, and regularly review their repayment strategy.

The SAVE Plan, particularly with its 10-year forgiveness timeline for lower balances and significantly reduced payments, offers a powerful tool for financial empowerment. By understanding its mechanics, maximizing its benefits, and diligently managing your enrollment, you can navigate your student loan debt with greater confidence and work towards a future free from this financial burden.

Don’t wait until 2026 to start planning. Take action now to assess your eligibility, understand your options, and make the best decisions for your student loans. Your financial future depends on it.